AI Automation for Insurance Claims and Underwriting

Your claims team is still processing first notices of loss by hand. Your underwriters spend hours chasing documents before they can make a single decision. And your compliance team is one regulatory change away from another manual re-engineering project.

This isn't a talent problem. It's a workflow problem. And across all insurance lines - from personal auto to specialty risk - the gap between what AI-powered automation can deliver and what most carriers are running has never been wider.

This guide covers the complete automation stack for insurance operations: underwriting, claims processing, fraud detection, policy management, and risk assessment — with the security and governance architecture that regulated carriers require.

Key facts driving urgency:

- Insurance companies implementing AI workflows see a 60% reduction in claims processing time and a 40% decrease in error rates

- Claims handlers spend roughly 30% of their time on low-value, repetitive tasks like document review and data entry

- 60% of policyholders cite slow claim settlement as a significant concern

- Approximately 10% of property and casualty insurance claims are fraudulent, costing the industry billions annually

- Over 65% of insurance professionals are planning substantial AI investments in the near term

1. Why Insurance Workflow Automation Is No Longer Optional

The insurance industry is caught between two pressures that pull in opposite directions. On one side: policyholders who expect fast, digital-first experiences — claims resolved in hours, not weeks. On the other hand, regulators who demand documented, auditable processes for every decision. Manual workflows can't satisfy both simultaneously.

The competitive threat is real and accelerating. Insurtech firms like Lemonade have built entire business models around AI-driven underwriting. Established carriers like Allstate are integrating AI into their risk assessment pipelines. The carriers that are still running manual intake forms, paper-based claims, and spreadsheet policy trackers aren't just inefficient — they're losing policyholders to competitors who can deliver answers in minutes.

But the compliance requirement cuts both ways. Insurance is one of the most heavily regulated industries in the world, with requirements varying by state, line of business, and customer segment. Automation that moves fast without leaving a traceable audit trail isn't a solution — it'sa liability. The answer is governed by automation: workflows that are fast, accurate, and fully explainable to regulators.

2. The Core Challenges Facing Insurance IT & Operations Teams

Fragmented Tools and Manual Handoffs

The real problem in insurance operations isn't a lack of technology — it's the gap between tools. When claims intake, document review, approval routing, and storage all live in separate systems, you don't have a workflow; you have a relay race where the baton gets dropped constantly. Each handoff introduces latency, miscommunication, and potential errors.

As one practitioner described it: "Many insurance teams still rely on fragmented tools and manual review processes, which slow down approvals and increase the chances of errors or missed risks." The solution isn't a better standalone tool — it's a connected workflow that handles the entire process as a unified system.

The Generic Tool Problem

Off-the-shelf automation platforms were built for marketing teams to automate email sequences, not claims departments handling regulatory complexity. Insurance terminology is specific. Saying the wrong thing creates liability. And most generic tools fail immediately when they encounter the edge cases — the contested claim, the specialty risk submission, the multi-jurisdiction policy — that make insurance operations genuinely complex.

Legacy Infrastructure

Most insurance carriers run policy administration systems that weren't designed for API-first integration. They lack the modern connectivity that contemporary AI tools require. And replacing them isn't realistic — these systems encode years of business logic and regulatory configuration that simply can't be rebuilt overnight.

The answer is the same as in banking: an intelligent middleware layer that wraps legacy systems in modern API capabilities, handling data in both directions without touching the core infrastructure.

3. Underwriting Automation

Underwriting is where the complexity of insurance operations is most concentrated — and where automation delivers some of its highest ROI. For standard admitted lines, the opportunity is throughput. For specialty risks, the opportunity is augmentation.

Standard Lines: Automating the High-Volume Cases

For personal auto, homeowners, and basic commercial liability, most submissions follow predictable patterns. An AI-powered underwriting workflow handles these automatically:

- Trigger: New submission received via portal or API

- Data validation and enrichment: Required fields checked, third-party data pulled (credit scores, property records, claims history)

- AI risk scoring: Composite risk score generated based on your institution's specific underwriting criteria

- Conditional routing: Low-risk submissions auto-quoted and issued; medium-risk flagged for junior underwriter review; high-risk escalated to senior underwriter

- Compliance check: NAIC requirements, state Department of Insurance rules, and fair underwriting standards verified automatically

- Decision and communication: Approved submissions trigger automated quote generation; declined submissions generate compliant adverse action notices

The results are significant: automation can handle 70–80% of standard submissions without human involvement, compressing quote turnaround from day to minute.

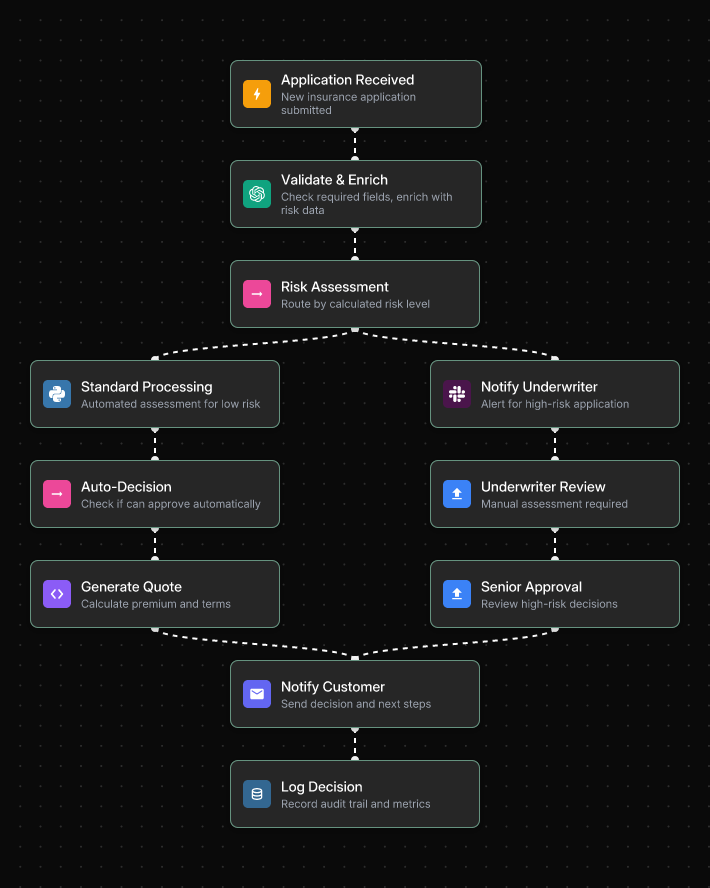

Here is what an automated underwriting workflow looks like in Jinba Flow — routing applications based on risk level, generating quotes automatically for low-risk cases, and escalating high-risk applications to senior underwriters:

Low-risk applications move through standard processing and auto-decision without any human involvement. High-risk applications are immediately flagged to the underwriter with full context pre-packaged — so the underwriter opens a file ready to decide, not ready to gather data.

Specialty Lines: Augmenting Expert Judgment

Specialty insurance — cyber, marine, engineering, fine art, kidnap and ransom — is where AI augments rather than replaces underwriter expertise. These risks don't have neat actuarial tables. They rely on the underwriter's knowledge, experience, and judgment.

The automation opportunity in specialty lines isn't decision-making — it's process burden elimination. Policy issuance can take an hour per client in complex cases due to coordination requirements, compliance checks, and manual data gathering. AI workflows address this by:

- Codifying expert decision trees into structured, digital workflows

- Automating data enrichment — pulling contractor safety records, financial filings, environmental compliance data via API before the underwriter opens the file

- Enforcing consistent compliance and audit trails for every submission

- Routing applications based on complexity so simple submissions move fast and complex ones reach the right expert immediately

The underwriter's time is freed for the work that requires expertise: analyzing novel risks, exercising judgment, and building the broker relationships that close deals.

→ See also: How to Automate Underwriting While Maintaining Compliance (Enterprise Guide)

→ See also: Digital Insurance Underwriting Solutions for Specialty Risks and Complex Policies

4. Claims Processing Automation

Claims are where policyholders form their lasting impression of your brand. A slow, opaque claims experience — even after a fair settlement — erodes trust in ways that no marketing campaign can recover. AI-powered claims workflows don't just reduce costs. They change what the policyholder experience feels like.

The Seven-Stage Claims Workflow

A complete automated claims management system covers every stage from first notice of loss to final settlement:

- FNOL and data ingestion: Claims accepted through multiple channels — web forms, mobile apps, email, API — feeding into a single structured pipeline. OCR extracts key data from uploaded documents. Policy coverage verified automatically before any human touches the claim.

- Smart routing and triage: Conditional logic assigns each claim to the right path immediately. A $500 windshield replacement and a $2 million property loss require different handling — smart routing applies the correct process to each without manual triage.

- Configurable adjudication logic: Coverage, deductibles, and policy limits checked automatically. AI models trained on historical claims data suggest fair settlement ranges, ensuring consistency across adjusters.

- Proactive fraud detection: Risk scoring runs in parallel with other evaluation steps. Claims above the fraud threshold pause for Special Investigations Unit review with a pre-packaged flag summary.

- Automated approvals and payments: Once adjudication rules are satisfied and fraud score is within acceptable bounds, payment initiation triggers automatically via API to your payment system.

- Policyholder communications: Automated updates sent at every milestone — claim received, under review, approved, payment sent. Proactive communication improves satisfaction even when outcomes aren't ideal.

- Audit trails: Every decision, action, and timestamp logged automatically. Every step of the adjudication logic recorded for regulatory review.

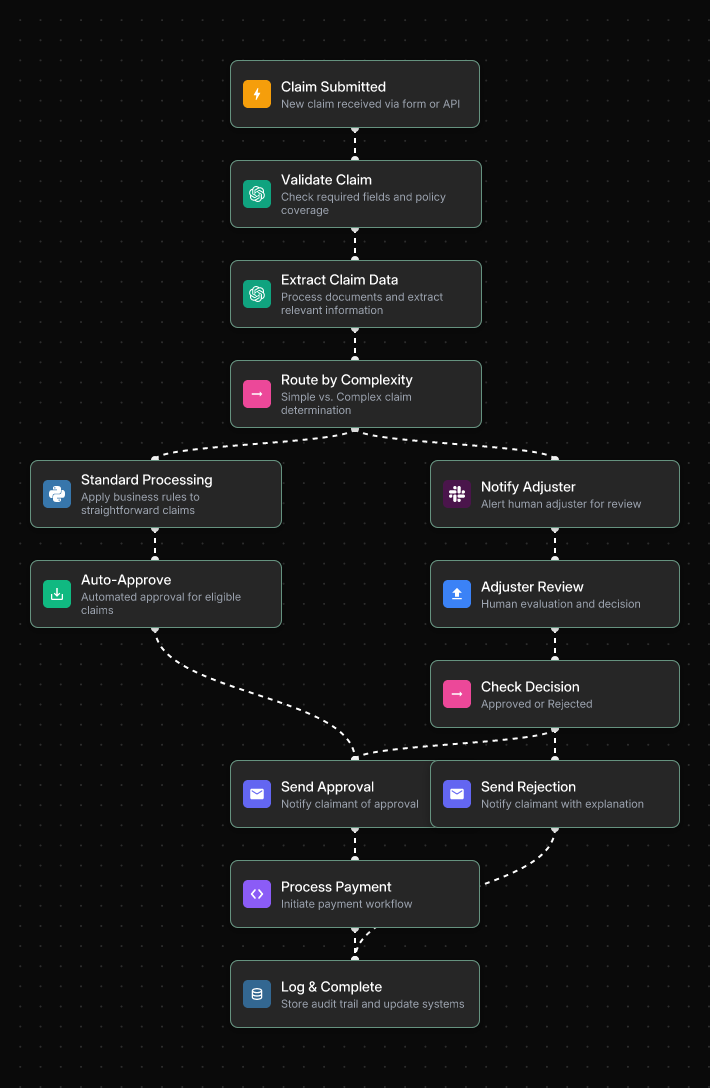

The following workflow shows how a complete claims processing pipeline operates in Jinba Flow — from initial submission through complexity-based routing, adjuster review, payment processing, and final audit logging:

Simple claims are auto-approved and proceed directly to payment. Complex claims trigger an adjuster notification with all extracted claim data pre-loaded — eliminating the manual document gathering that typically delays adjuster decisions by days.Real-World Impact

Insurance companies implementing AI-powered claims workflows report a 60% reduction in processing time and a 40% decrease in error rates. One South American insurer piloting generative AI for claims intake tasks saw productivity improve by up to 50%. The reason these numbers are achievable is straightforward: automation eliminates manual bottlenecks that account for most processing time.

→ See also: 7 Ways to Build an Insurance Claims Workflow with Automation (2026 Guide)

→ See also: How to Implement AI Claims Processing Without IT Bottlenecks

→ See also: 7 AI Claims Processing Solutions Compared: Build vs Buy Analysis for 2026

5. Fraud Detection in Insurance

Approximately 10% of property and casualty insurance claims are fraudulent, costing the industry billions annually. The challenge is that fraud rarely announces itself — it hides patterns that are invisible to a manually-reviewed claim but detectable at scale with the right signals.

What AI Detects That Rules Miss

Static rule-based systems catch known fraud patterns. AI behavioral analysis catches patternyour rules have never seen — and it gets smarter over time. A fraud detection workflow integrates a risk scoring model that evaluates each claim against behavioral and contextual signals:

- Multiple claims filed within a short window

- Inconsistencies between the incident description and supporting documents

- Claimants or providers appearing on watchlists

- Suspicious billing patterns in medical claims

- Unusual claim amounts relative to the reported incident

Tiered Response Architecture

When a claim risk score exceeds a defined threshold, the workflow pauses automatic processing and routes it to the Special Investigations Unit with a summary of the specific flags triggered — giving investigators a head starts rather than a cold file. This fraud detection step runs in parallel with other evaluation steps, so it doesn't add latency to most clean claims.

Real-world implementations of this architecture have achieved a 35% reduction in false positives within the first quarter of deployment, along with a 40% decrease in manual review volume.

→ See also: How to Implement Automated Risk Assessment in Insurance Operations

6. Policy Management & Compliance

After the claim is settled and the policy is issued, the compliance work is just beginning. Policy management — tracking renewals, managing attestations, maintaining audit-ready documentation — consumes thousands of hours annually in most insurance operations. And a single missed renewal or outdated policy creates material compliance exposure.

The Manual Policy Management Problem

Organizations managing policies typically lose 225 hours per year on policy management tasks, 750 hours chasing attestations and signoffs, and 2,000 hours on employees simply searching for the correct policy. Organizations with automated policy management see a 50% decrease in compliance violations.

Automated Policy Lifecycle Management

A complete automated policy management workflow covers the full lifecycle:

- Development: Regulatory feed flags a new requirement → task automatically created for policy owner

- Review and approval: Draft routed to stakeholders in defined sequence → approvals logged digitally

- Distribution: Final policy distributed to relevant employees via email and Slack notification

- Attestation tracking: Employees notified of required acknowledgments; completion tracked automatically

- Renewal monitoring: Automated reminders sent 90, 60, and 30 days before renewal deadlines

- Evidence collection: Scheduled workflows collect compliance evidence and attach it to the relevant control

- Audit readiness: Every action captured in an immutable audit log — available on demand, no scramble required

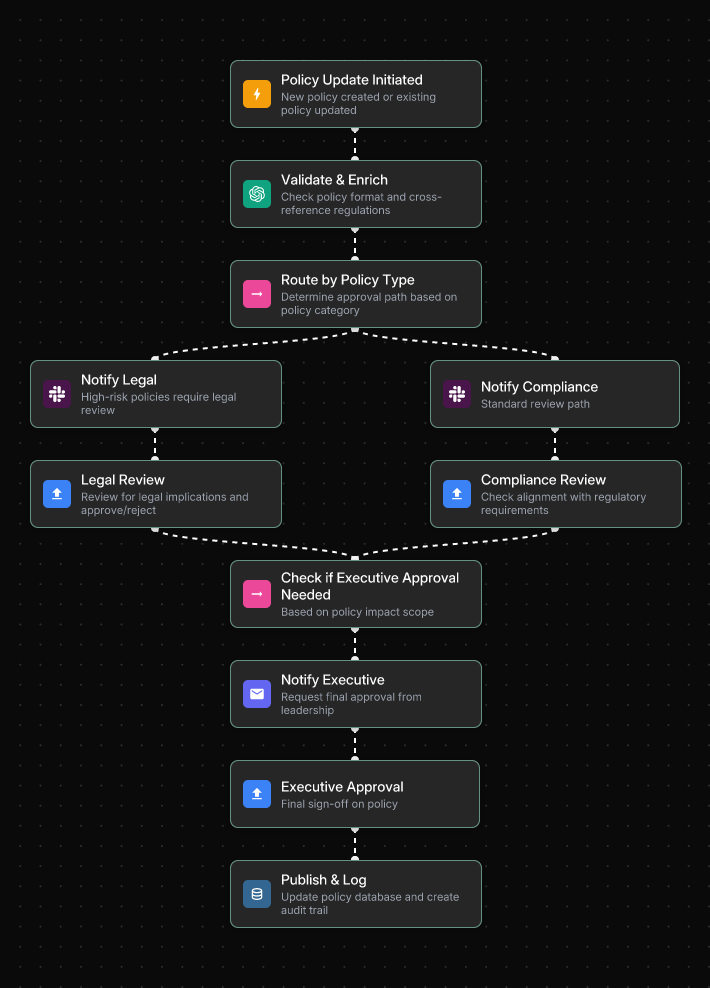

Here is what an automated policy management workflow looks like in Jinba Flow — routing by policy type, enforcing legal and compliance review, and triggering executive approval when the policy impact scope requires it:

High-risk policy changes route to Legal for review. Standard updates go directly to Compliance. Both paths converge at the executive approval gate when required — and every action is published to the policy database with a complete audit trail automatically.

GRC Stack Integration

Modern policy management automation doesn't replace your existing GRC platform — it connects to it. Workflows built on an orchestration layer can push policy status updates to Audit Board, SAP GRC, or Logic Gate; trigger acknowledgment tasks in your HRIS; and log compliance evidence automatically. The result: your policy management process becomes a continuous function rather than a periodic scramble.

→ See also: How to Automate Policy Management Workflows in 4 Weeks

→ See also: Policy Management Automation that Integrates with Your Existing GRC Stack

7. Risk Assessment Automation

Risk assessment sits at the heart of every insurance operation — underwriting, claims, reserving, and capital management all depend on accurate, consistent risk evaluation. Manual risk assessment is slow, inconsistent, and difficult to audit. Automated risk assessment is faster, more consistent, and fully traceable.

The Five-Step Implementation Framework

- Step 1 — Workflow analysis: Document every step of your current risk assessment process. Map every handoff, every decision point, every place where a human touches the file. Identify bottlenecks and establish baseline metrics.

- Step 2 — Data requirements: Identify all data sources — applicant information, historical claims, CRM records, third-party data. Audit for completeness and accuracy before automating processes that depend on it.

- Step 3 — Platform selection: Generic automation tools fail in insurance. Compliance requirements filter them out immediately. Look for platforms with SOC 2 compliance, private hosting, SSO, RBAC, audit logging, and private AI model hosting.

- Step 4 — Compliance integration: Embed compliance checks into the workflow from day one — not as a post-hoc review. Every automated decision must be logged in a tamper-evident audit trail. SHAP-based explanations make AI-driven decisions defensible to regulators.

- Step 5 — Change management: The best-designed automation system will fail if your team doesn't adopt it. Frame automation as eliminating the tedious work, so underwriters can focus on the complex cases that require their expertise.

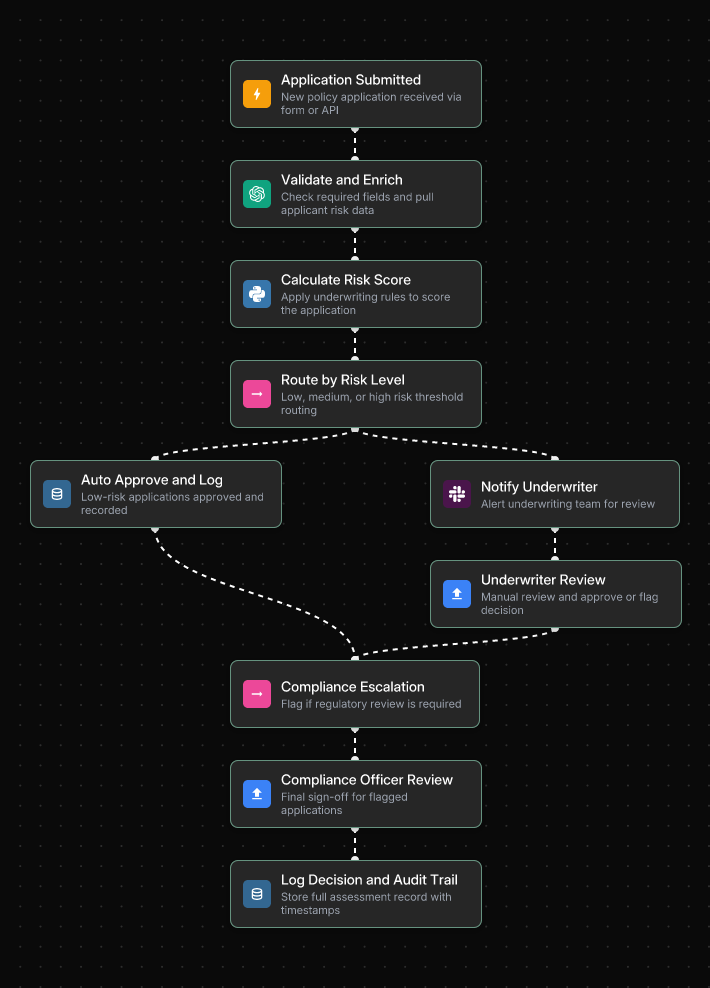

Below is an example of a risk assessment workflow built in Jinba Flow — calculating a risk score from applicant data, routing by risk level, and escalating to compliance officer review when regulatory sign-off is required:

Every decision path — auto-approve, underwriter review, or compliance escalation — feeds into the same audit trail, ensuring every risk assessment is fully documented regardless of which path it took.

→ See also: How to Implement Automated Risk Assessment in Insurance Operations

8. Security & Governance Architecture

Insurance operations handle some of the most sensitive data in any industry: personal health information, financial records, litigation history, and proprietary risk models. Any automation platform must meet the security requirements that this data demands.

Enterprise Security Requirements

- SOC 2 Type II compliance: Demonstrates controls operating consistently over 6–12 months. Standard enterprise carriers and reinsurers require — not a point-in-time snapshot.

- On-premises and private cloud hosting: Sensitive policyholder data cannot be routed through shared public infrastructure. Private deployment keeps your data within your controlled perimeter.

- SSO + RBAC: Claims handlers execute workflows without being able to modify them. Compliance officers audit without being able to approve. Every role has exactly the access it needs — nothing more.

- Immutable audit logging: Every workflow execution logged automatically — inputs, outputs, decision branches, timestamps, user IDs. Your evidence trails for regulatory examinations and litigation discovery.

- Private AI model hosting: Via AWS Bedrock, Azure AI, or self-hosted models. Policyholder data and proprietary risk models never pass through a public AI API.

Build vs. Run Separation

The governance principle that matters most in insurance automation is separating who builds workflows from who runs them. Technical teams and compliance architects design and govern workflows in a builder interface. Claims handlers, underwriting assistants, and ops staff execute approved workflows through a controlled interface — without any risk of accidentally modifyingthe underlying adjudication logic or compliance rules.

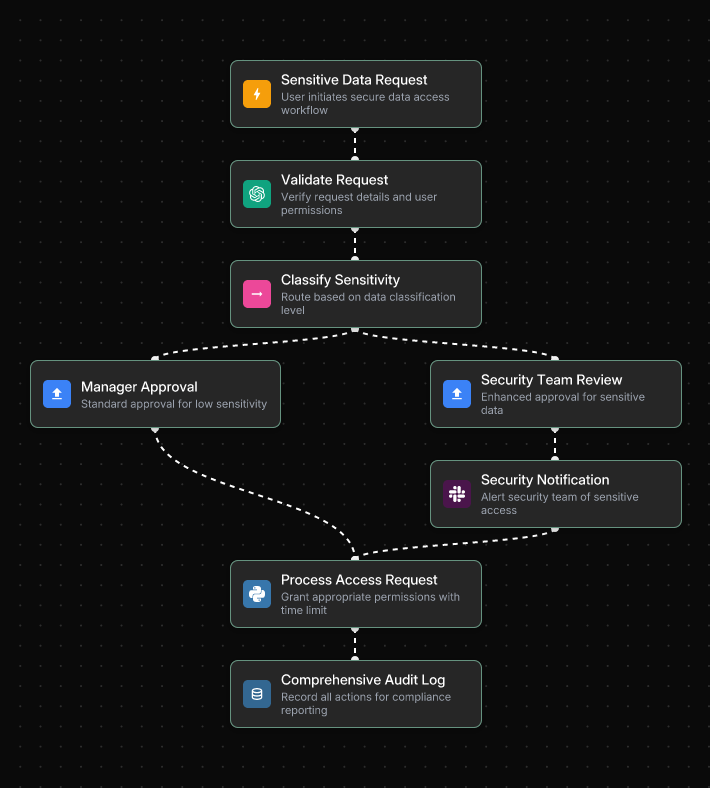

The following workflow demonstrates how sensitive data access requests are governed in Jinba Flow — classifying by sensitivity level, applying the appropriate approval path, and generating a comprehensive audit log for every access event:

Standard requests receive manager approval and proceed automatically. Sensitive data requests trigger an additional security team review and notification before access is granted — ensuring no sensitive data is accessed outside of a fully documented, approved process.

This separation is what makes enterprise-grade automation genuinely safe to deploy across a distributed claims or underwriting operation.

→ See also: AI Workflow Automation for Regulated Industries: Compliance Guide

→ See also: Top 5 SOC 2 Workflow Automation Tools for Enterprise

9. Implementation Roadmap

The insurance carriers succeeding with automation share one characteristic: they start with a single, well-scoped process, prove the value, and expand systematically. The instinct to automate everything at once consistently leads to failure.

- Phase 1 — Assessment (Weeks 1–4): Map your highest-pain manual process. For most carriers, this is FNOL intake or underwriting document collection — high frequency, measurable ROI, lower compliance risk for a first deployment. Document the current process step by step. Establish baseline metrics for processing time, error rate, and cost per case.

- Phase 2 — Build and pilot (Weeks 5–10): Describe the workflow in plain language to generate an initial draft automatically. Refine in the visual editor — add conditional logic, compliance checks, and system integrations. Test against your messiest real cases. Pilot with a small group before full rollout. Frame the change internally as eliminating tedious work, not replacing expertise.

- Phase 3 — Deploy and measure (Weeks 11–16): Publish as a production-ready API that integrates with your existing policy administration system or claims platform. Track processing time reduction, error rate improvement, and cost per case. Use early results to build the business case for expansion.

- Phase 4 — Scale (Weeks 17+): Expand additional claim types, underwriting lines, or operational functions. Integrate with additional channels and data sources. Establish a quarterly model of retraining and workflow optimization cadence.

→ See also: How to Implement Automated Risk Assessment in Insurance Operations

10. Getting Started with Jinba Flow

Jinba Flow is a YC-backed, SOC II compliant AI workflow builder purpose-built for Fortune 500 enterprises. With over 40,000 enterprise users running automated workflows daily, it's designed specifically for the complexity that insurance operations demand — multi-step workflows, compliance requirements, legacy system integration, and the need for a clean separation between building and running.

Why Jinba for Insurance Automation

- Chat-to-Flow Generation: Describe your claims or underwriting workflow in plain language — Jinba generates a working draft automatically. No developer required. No engineering backlog. Describe "When a new FNOL arrives, validate coverage, route to the correct adjuster, and send an acknowledgment to the policyholder" and have a production-ready workflow in minutes.

- Visual Workflow Editor: Every adjudication rule, every conditional branch, every escalation path visible as a flowchart. Compliance teams can audit the logic. Regulators can understand the process. No black boxes.

- Deploy as API or MCP Server: Workflows publish as reusable endpoints that integrate with your existing policy administration system, claims platform, or CRM — without rebuilding infrastructure.

- Evidence by design: Every execution logged automatically — inputs, outputs, decision branches, timestamps. Audit-ready case files as a byproduct of the workflow, not an afterthought.

- Jinba App for non-technical execution: Claims handlers, underwriting assistants, and ops staff execute approved workflows through a simple chat interface. No custom UI. No risk of modifying adjudication logic.

- SOC 2 + private hosting: On-prem and private cloud deployment. Private model hosting via AWS Bedrock, Azure AI, or self-hosted. Policyholder data never touches a public API.

Your First Workflow to Build

Start with FNOL intake automation or underwriting document collection — high volume, clear ROI, and manageable compliance risk for a first deployment. From there: automated adjudication logic, fraud scoring integration, policy renewal tracking, and multi-line expansion.

The carriers that will lead in the next decade aren't the ones who automated everything at once. They're the ones who built one governed, auditable workflow, proved the value, and scaled from there.

Frequently Asked Questions

What is insurance workflow automation?

Insurance workflow automation uses AI and workflow software to handle the repetitive, rules-based tasks across insurance operations — FNOL intake, document processing, underwriting routing, claims adjudication, fraud scoring, and policy management — without manual intervention for standard cases. The goal is not to replace adjusters or underwriters but to free them from administrative work so they can focus on the complex cases that require their expertise.

How does AI improve claims processing?

AI improves claims processing by executing in parallel what humans do sequentially. FNOL data extraction, coverage verification, fraud scoring, and adjuster routing can all happen simultaneously in an automated workflow — compressing days of back-and-forth into minutes. Leading implementations report a 60% reduction in processing time and a 40% decrease in error rates.

Can AI handle specialty insurance underwriting?

AI augments specialty insurance underwriting rather than replacing it. For specialty risks — cyber, marine, engineering, fine art — the underwriter's expertise and judgment remain essential. AI handles the process burden: pulling data, checking compliance, routing submissions, and building pre-packaged case files. This frees underwriters to focus on the high-value analytical, and relationship work that requires their expertise.

How do I ensure AI-driven insurance decisions are compliant?

Compliance requires that every automated decision be explainable, auditable, and traceable. This means choosing a platform with immutable audit logging, visual workflow logic rather than opaque ML models, built-in compliance check steps for NAIC requirements and state DOI rules, and enterprise security standards: SOC 2 Type II, private hosting, SSO, and RBAC.

What is the ROI of insurance workflow automation?

ROI varies by function and automation scope. For claims processing, a 60% reduction in cycle time and 40% fewer errors are consistent benchmarks. For underwriting, automating 70–80% of standard submissions eliminate the administrative drag that consumes junior underwriter time. For policy management, a 50% reduction in compliance violations is a documented outcome of moving from manual to automated processes.

Will AI replace claims adjusters and underwriters?

No — and that's not the goal. AI handles the 70–80% of insurance operations that ismechanical, rules-based, and consistent. Claims adjusters handle contested liability, complex bodily injury, and the human moments when a policyholder needs to feel heard. Underwriters handle new business risks, nuanced judgment calls, and broker relationships. Automation makes both more productive — it doesn't eliminate the need for their expertise.

The Bottom Line

The insurance industry is at an inflection point. Policyholders expect fast, digital-first experiences. Regulators expect documented, auditable processes. Insurtech competitors are delivering both simultaneously. Manual workflows can't keep up with any of these demands.

The carriers closing this gap aren't doing it by replacing their people or their core systems. They're doing it by building an intelligent automation layer on top of what they already have — handling the high-volume mechanical work, producing audit-ready case files automatically, and routing the genuinely complex cases to the humans who can make the best decisions.

Start with one workflow. Build the audit trail in from day one. Scale from there.