AI Workflows for Bank and Loan Automation

Traditional loan processing takes 30 to 60 days. Fintechs approve accounts in minutes. The gap is not a technology problem — it is a workflow problem. This guide covers the complete automation stack for banks and credit unions: from digital account opening through loan origination, credit decisioning, fraud prevention, and compliance.

Key facts driving urgency:

- Only 50% of national banks support full mobile account opening vs. 91% of fintechs

- AI-driven workflows can cut loan processing times by 60%+ and reduce credit risk by up to 70%

- 20% of applicants abandon loan applications if the process takes too long

- 45% of digitally acquired accounts close within 3 months when onboarding is poor

1. The Core Challenges Facing Bank IT & Operations Teams

Before diving into solutions, it is worth naming the obstacles that make banking automation difficult.

Legacy System Integration

Most core banking platforms lack modern APIs. The instinct is to replace everything — but rip-and-replace is expensive, risky, and destroys institutional knowledge. The smarter path is an API middleware layer: build a wrapper that sits between your legacy system and modern AI capabilities, handling data in both directions without touching the core. Your LOS calls a workflow endpoint, gets an enriched decision back, and continues operating normally.

Compliance & Regulatory Requirements

FCRA, ECOA, TILA, AML rules — every automated decision must be explainable, auditable, and traceable. "The model said no" is not an acceptable adverse action reason. This is why your automation platform's architecture matters: visual workflow logic is more auditable than opaque ML models.

Speed vs. Accuracy

50% of applicants will not tolerate more than 10 application questions. Yet a single pricing error in a commercial loan can cost more than the deal is worth. The hybrid model resolves this tension: automate 70–90% of standard decisions, route complex cases to human review.

2. Digital Account Opening Automation

The account opening experience is the first real test of your digital infrastructure — and the most common failure point.

The Thin-File Problem

Younger applicants, new immigrants, and people who have operated primarily in cash have little footprint in traditional credit databases. When automated systems cannot find them in the bureaus, they default to a branch referral — which is a conversion killer. The applicant who wanted to open an account at 11 PM is not going to a branch on Tuesday morning.

AI-Powered Identity Verification

Modern verification layers multiple signals in parallel: OCR document scanning, biometric facial recognition, and multi-source cross-referencing against alternative data (utility records, telecom data). Leading systems achieve 95% detection rates with a 50% reduction in false positives — expanding digital approvals to thin-file applicants without compromising fraud prevention.

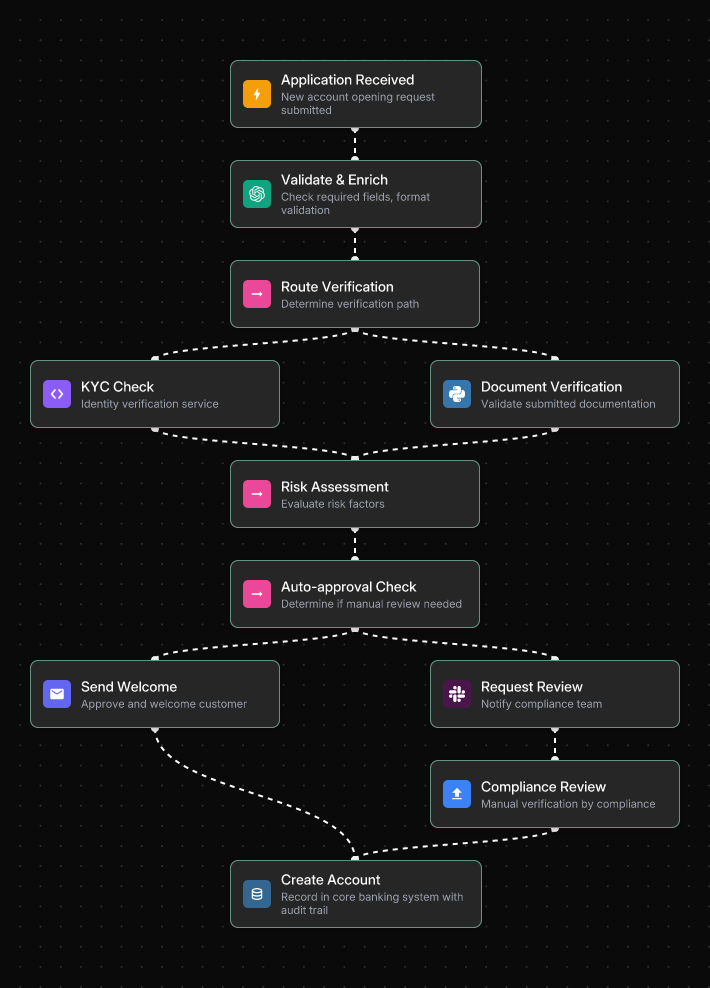

Here is what a complete digital account opening workflow looks like when built in Jinba Flow — from initial application intake through KYC verification, risk assessment, and final account creation:

Notice how the workflow branches automatically based on the auto-approval check — clean applications receive a welcome email instantly, while flagged cases are routed to the compliance team for manual review, without any manual triage required.

Onboarding as a Revenue Driver

Personalized onboarding improves retention by 10% year-on-year and generates over $1,000 in incremental lifetime value for high-balance customers. The onboarding moment is one of the highest-intent interactions a customer will have with your institution — AI workflows can turn it into a targeted cross-sell opportunity.

→ See also: How Fortune 500 Banks Streamline Digital Account Opening with AI Workflows

3. Loan Origination & Processing: Five Automation Stages

AI-driven workflows can cut loan processing times by over 60% when applied to the right stages. Here is where the time goes - and where automation eliminates it.

- Document Extraction & Verification: OCR + AI extracts structured data from any document type. 50%+ reduction in collection time. Missing documents triggers automatic applicant notifications.

- Credit Scoring & Risk Assessment: Real-time bureau pulls + alternative data sources. 20% reduction in bad debtexposure. 80–90% automation for low-risk profiles.

- Eligibility Calculation: DTI, LTV, credit score thresholds applied automatically against current product guidelines. ~60% faster assessment.

- Compliance Checks: OFAC, AML, Fair Lending checks run in parallel — not sequentially. 70% faster verification, 100% rule coverage.

- Final Approval & Signing: Risk-based routing to correct approver, automatic e-signature integration. Up to 4x faster. A 30–60-day process reduced to days or hours for standard applications.

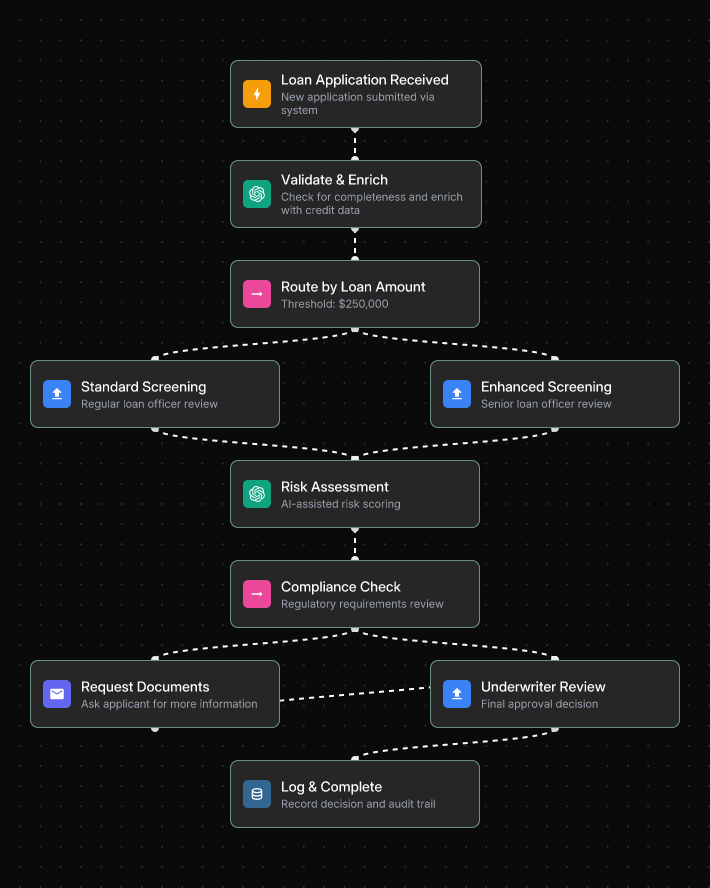

The following workflow shows how a loan screening process can be fully automated in Jinba Flow — routing applications based on loan amount, running AI-assisted risk scoring, and escalating to human underwriters only when needed:

The key design principle here is the $250,000 threshold that triggers enhanced screening — standard applications move through automatically, while large or complex loans get the additional scrutiny they require.

→ See also: 5 AI-Powered Loan Processing Workflows That Reduce Approval Time by 70%

→ See also: Automate Loan Processing with AI: ROI Calculator & Implementation Roadmap

→ See also: Loan Origination Automation for Regional Banks and Credit Unions

4. AI Credit Decisioning: Build, Buy, or Hybrid?

The credit decision is the most consequential step in the loan lifecycle — and the one where the compliance stakes are highest.

The Three Approaches

- Build from scratch: Complete customization, full IP ownership. But break-even typically takes 2.7+ years and $500K+. Not the right choice for most institutions.

- Buy off-the-shelf: Faster to market, but limited customization — and most platforms still do not solve the explainability gap regulators require.

- Hybrid build-on-buy: Automate 60–70% of decisions for clear-cut cases, route complex applications to human review. This is the approach practitioners consistently recommend as the sweet spot.

Closing the Explainability Gap

FCRA requires specific documented reasons for every adverse action. A visual workflow editor — where every decision branch and rule condition is laid out as a readable flowchart — is inherently more auditable than an opaque model. When an examiner asks how a credit decision was reached, you can walk them through the logic step by step.

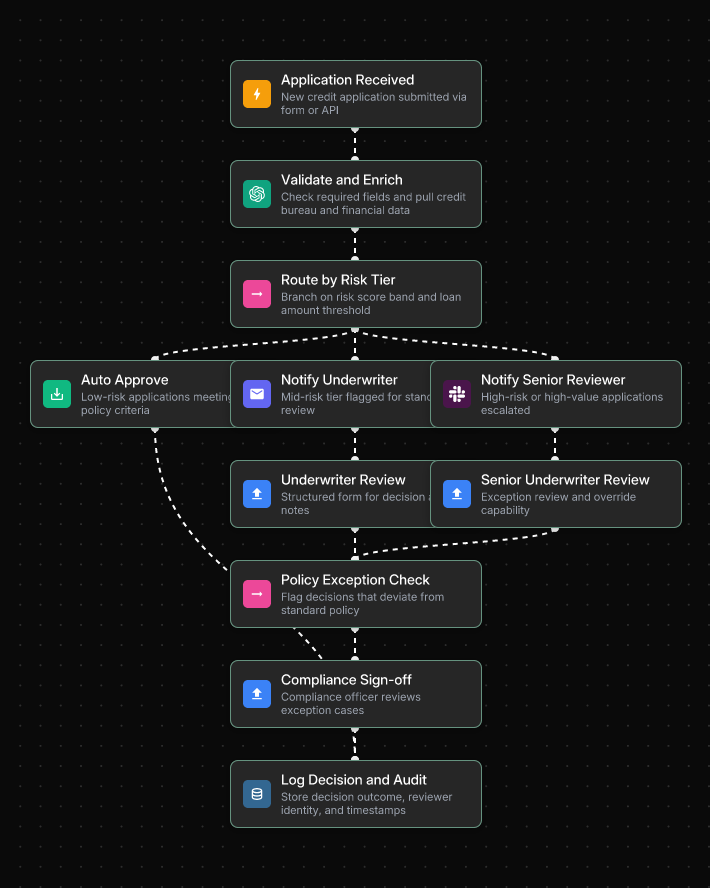

Below is an example of a credit decision workflow built in Jinba Flow — applying risk-tier routing, human-in-the-loop review for mid and high-risk applications, and a full compliance sign-off layer before final decision:

Every decision path — auto-approve, underwriter review, or senior escalation — feeds into the same audit log, ensuring every credit decision is fully traceable regardless of which path it took.

Specialized Models by Loan Type

A mortgage application requires different data, risk signals, and compliance logic than a microloan. Treating all loan types the same is the most common cause of lending automation failure. Each category — mortgage, personal, auto, commercial, microloan — needs its own purpose-built workflow.

→ See also: Building vs. Buying an AI Credit Decision Builder: The Complete ROI Analysis

→ See also: How to Build an AI Credit Decision Engine with No-Code Workflows

→ See also: 5 AI Workflow Models to Automate Loan Approval for Different Lending Types

5. Fraud Detection & Bank Account Verification

Even a valid, active bank account can be a fraud risk. Chargebacks that eat 4% of revenue do not announce themselves — they accumulate quietly. Smarter, layered automation catches fraud signals before they cost you.

Verification Methods: A Quick Comparison

- Instant Account Verification (IAV): 30–60 seconds, ~$1.50/verification, ~5% drop-off. Fast, but users distrust credential sharing.

- Micro-deposits: Most trusted method, ~$0.75/verification, 1–3-day delay, up to 20% drop-off.

- Prenote/ACH: B2B standard. Zero-dollar test transaction validates account before real money moves.

- Risk-adaptive hybrid: Default to IAV, automatically fall back to micro-deposits if unavailable. Well-designed hybrid setups cut chargebacks by 80%.

Enterprise Fraud Detection Workflow

Dynamic fraud scoring (0.0–1.0 risk score) enables tiered routing: auto-approve, review queue, or immediate SIU escalation. Fraud scoring runs in parallel with other evaluation steps — clean cases are not delayed. Real-world implementations have achieved a 35% reduction in false positives within the first quarter of deployment.

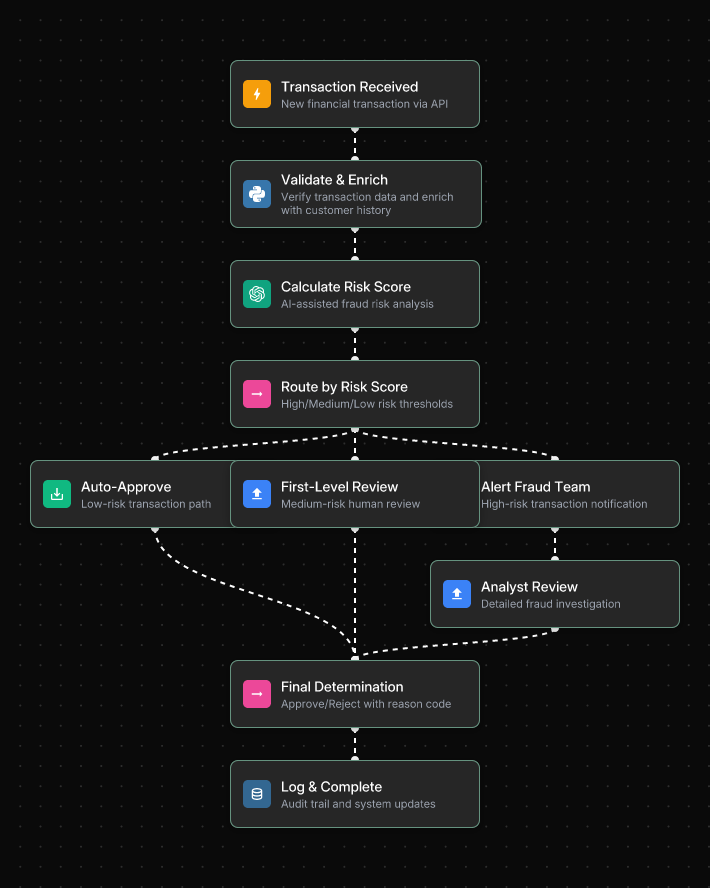

Here is how a fraud detection workflow operates in Jinba Flow — running AI-assisted risk scoring on every transaction and routing automatically based on risk level, so analysts only handle the cases that genuinely require their attention:

The three-path routing — auto-approve, first-level review, and immediate fraud team alert — means clean transactions are never delayed while high-risk cases receive immediate escalation.

→ See also: 7 Steps to Build an Enterprise-Grade Fraud Detection Workflow

→ See also: 7 Bank Account Verification Workflows That Prevent Fraud

→ See also: How to Build a Bank Account Verification Workflow That Scales

6. Compliance & Security: The Non-Negotiables

For IT and security teams at financial institutions, compliance is not a feature — it is a prerequisite. Any platform that does not meet these requirements does not make the shortlist.

Enterprise Security Requirements

- SOC 2 Type II compliance: Not Type I. Type II demonstrates controls operating consistently over 6–12 months — the standard enterprise partners require.

- On-premises and private cloud hosting: Sensitive financial data cannot be routed through shared public infrastructure.

- SSO + RBAC: Loan officers execute workflows without being able to modify them. Compliance officers audit without being able to approve.

- Immutable audit logging: Every execution — inputs, outputs, branches, timestamps, user IDs — logged automatically and tamper-proof.

- Private AI model hosting: Via AWS Bedrock, Azure AI, or self-hosted. Sensitive financial data never passes through a public AI API.

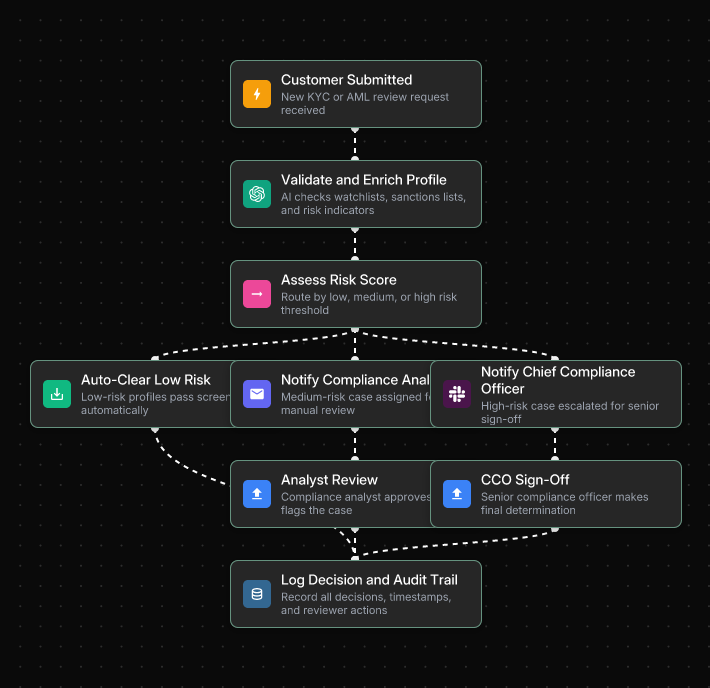

The following workflow shows how a KYC/AML screening process can be automated end-to-end in Jinba Flow — from initial watchlist and sanctions checks through risk-tiered routing to compliance analyst review and CCO sign-off:

Every action taken — from the initial AI screening to the final CCO decision — is recorded in an immutable audit log with timestamps and reviewer details, producing a defensible compliance record automatically.

Governance Architecture That Works

The critical design principle is separating the build and execution environments. Technical teams design and govern workflows in a builder interface. Business users — loan officers, processors, compliance staff — execute approved workflows through a controlled interface that does not expose the underlying logic. Every execution is logged. No accidental modifications. No governance gaps.

→ See also: AI Workflow Automation for Regulated Industries: Compliance Guide

→ See also: Top 5 SOC 2 Workflow Automation Tools for Enterprise

7. Implementation Roadmap

The banks that succeed with automation are not the ones with the biggest budgets. They are the ones with the most disciplined approach.

- Phase 1 — AI Readiness Assessment (Weeks 1–6): Data quality audit, infrastructure review, skills gap analysis. Do not skip this phase — it determines whether your investment delivers or disappoints.

- Phase 2 — Pilot Selection (Weeks 7–13): Define measurable KPIs before you build anything. Best first pilots: document verification or digital account opening — high volume, clear ROI, low compliance risk.

- Phase 3 — Build & Deploy (Weeks 14–26): Describe process in plain language → auto-generate workflow draft → refine in visual editor → test with real data → deploy as API endpoint. Your existing LOS calls the workflow an API. No migration is required.

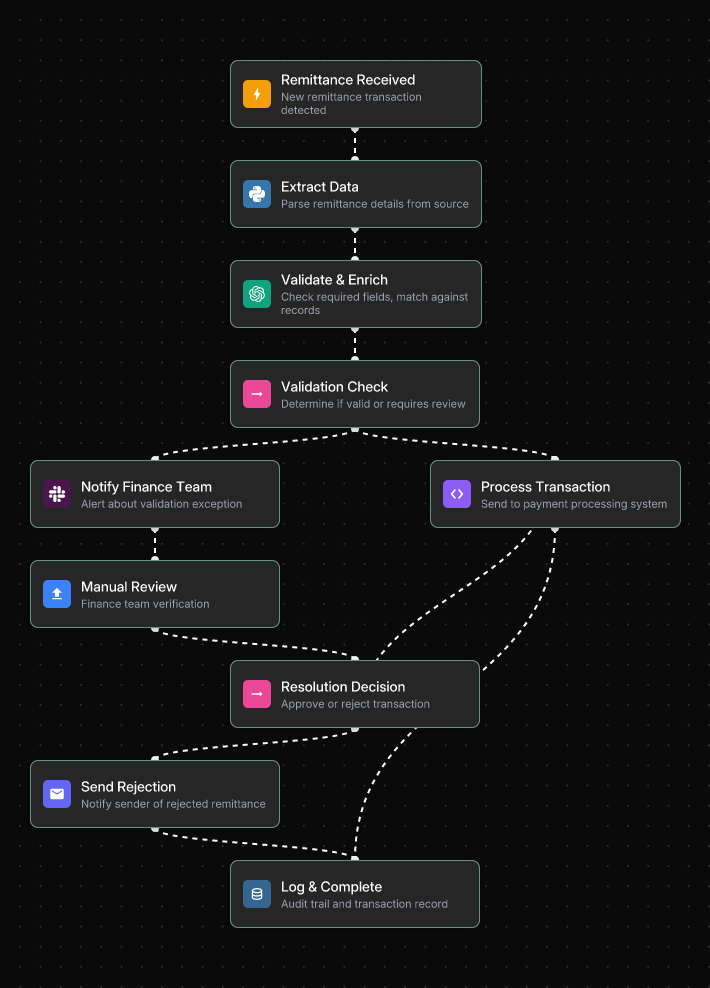

Below is an example of a remittance validation workflow in Jinba Flow — automatically parsing incoming remittance data, validating against records, and routing exceptions to the finance team for manual review:

When validation passes, the transaction moves directly to payment processing with no human involvement. When an exception is detected, the finance team receives an immediate alert with full context — eliminating the manual inbox monitoring that typically creates bottlenecks in AR operations.

- Phase 4 — Scale & Optimize (Weeks 27+): Use pilot results to build the business case for expansion. Establish quarterly model retraining cadence. Allocate 15–20% of ongoing AI ops for budget monitoring and improvement.

→ See also: How to Implement Manufacturing Process AI Automation in 90 Days or Less

8. ROI & Business Case

The most common obstacle to banking automation is not technical — it is the inability to translate AI investments into measurable returns. Here is the framework.

Simple ROI Calculation

- Annual labor savings = (Manual hours per loan − Automated hours per loan) × Annual loan volume × Fully loadedhourly rate

- Example: 500 loans/month, 5 hours manual work, $45/hour = $1.35M annual labor exposure. 50% reduction = $675K annual savings — before increased throughput and reduced fraud losses.

Benchmarks by Stage

- Document verification: 50%+ time reduction; processing drops from 30 to 14 days

- Credit scoring: Days → minutes; 20% reduction in bad debt exposure

- Compliance checks: 70% faster verification

- Final approval: Up to 4x faster

- Overall: 30–60-day process reduced to days or hours for standard applications

Real-World Case Study

A major US retail bank implementing AI automation for Tesla loans reported: 88% reduction in processing time, 45% increase in loan closings, 20% increase in underwriting margins, and 50% reduction in credit risk.

→ See also: Automate Loan Processing with AI: ROI Calculator & Implementation Roadmap

9. Getting Started with Jinba Flow

Jinba Flow is a YC-backed, SOC II compliant AI workflow builder purpose-built for Fortune 500 enterprises. With over 40,000 enterprise users running automated workflows daily, it is designed to bridge exactly the gap that banking IT teams face: powerful, governed automation that integrates with legacy systems without requiring a complete technology overhaul.

Why Jinba for Banking Automation

- Chat-to-Flow Generation: Describe your workflow in plain language — Jinba generates a working draft automatically. No developer is required to get started.

- Visual Workflow Editor: Every decision branch is visible as a flowchart. Compliance teams can audit logic. No black boxes.

- Deploy as API: Your existing LOS calls the workflow as an API endpoint. No migration. Legacy systems stay intact.

- SOC 2 + private hosting: Sensitive customer data never leaves your environment. Private model hosting via AWS Bedrock, Azure AI, or self-hosted.

- Build/run separation: Jinba Flow for technical teams to design. Jinba App for loan officers and ops staff to execute safely — without risk of modifying underlying logic.

Start with document verification or digital account opening. Prove ROI. Then expand.

Frequently Asked Questions

What is bank loan automation?

Bank loan automation uses AI and workflow software to handle the repetitive, rules-based tasks in lending — document collection, credit scoring, compliance checks, approval routing — without manual intervention for standard cases. The goal is not to replace underwriters but to free them for complex, high-value decisions.

Is AI-powered loan automation compliant with banking regulations?

Yes, when implemented correctly. Compliance requires that every automated decision be explainable, auditable, and traceable. This means choosing a platform with immutable audit logging, visual workflow logic (not opaque for ML models), built-in compliance check steps, SOC 2 Type II certification, private hosting, SSO, and RBAC.

How do I integrate AI automation with my existing legacy LOS?

Deploy automation workflows as secure API endpoints and configure your existing LOS to call those endpoints for specific decision steps. Your LOS sends application data; the workflow processes it and returns a structured response. No migration. No changes to your core banking platform.

Will AI replace loan underwriters?

No. AI handles the 70–80% of loan processing that is mechanical and rules-based. Human underwriters handle the 20–30% requiring judgment: complex financial situations, unusual risk profiles, and cases where regulatory accountability demands a documented human decision. Automation makes underwriters more productive — it does not eliminate the need for their expertise.

What is the ROI for bank loan automation?

For a mid-sized lender processing 500 loans per month, automation of key stages typically delivers $500,000 to $700,000 in annual labor savings alone, with payback periods under 24 months (about 2 years). Additional ROI comes from increased loan throughput, reduced fraud losses, and lower compliance overhead.

The Bottom Line

The competitive gap between banks and fintechs in digital lending is not a technology gap — it is a workflow gap. The tools to close it exist today, and they do not require replacing your core banking infrastructure.

The winning approach: an intelligent automation layer that sits on top of what you already have, handling the high-volume mechanical work while routing complex cases to human experts. SOC 2 compliant, privately hosted, fully auditable — and deployable as API endpoints your existing systems can call without any migration.

Start with one workflow. Prove the value. Built from there.